Stock futures are little changed as Wall Street starts the second half of 2023

U.S. stock futures showed little change on Monday morning, signaling a steady start to the second half of the year on Wall Street.

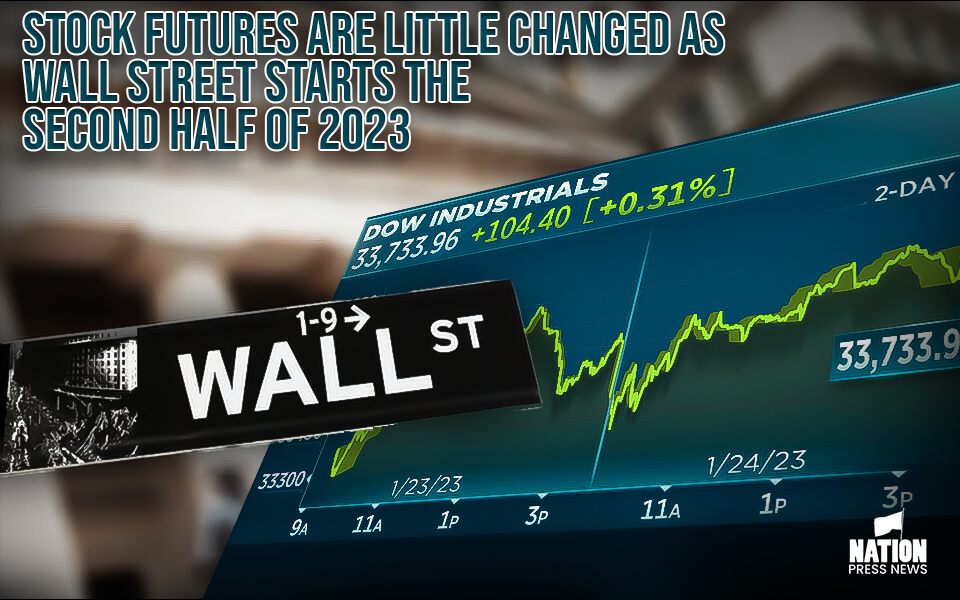

Futures tied to the Dow Jones Industrial Average decreased by 25 points, S&P 500 and Nasdaq-100 futures were the same when they closed.

Tesla shares remained relatively unchanged in overnight trading after the electric vehicle manufacturer reported delivery and production numbers that exceeded analysts’ expectations.

On the other hand, United shares saw a marginal decline due to flight disruptions caused by bad weather over the long holiday weekend.

The stock market had an exceptional start to 2023, with the Nasdaq Composite closing out its largest first-half gain since 1983, surging by 31.7%.

The S&P 500 also performed well, jumping 15.9% for its best first-half performance since 2019.

The Dow Jones Industrial Average lagged behind with a modest climb of 3.8% during the period.

The impressive gains can be attributed to the enthusiasm surrounding artificial intelligence, which boosted tech stocks.

Additionally, recent data showing a resilient U.S. economy despite higher interest rates alleviated concerns of an impending downturn and lifted investor sentiment.

Mark Hackett, Nationwide’s chief of investment research, noted that while the tailwinds from a technical perspective might be fading, there are indications of a potential shift from technical factors to fundamentals. Encouraging macro and earnings data suggest a possible transition that could further support market growth.

As the week began with a shortened trading schedule due to the Independence Day holiday, investors eagerly awaited the latest ISM Manufacturing PMI and S&P Global manufacturing PMI data for June.

These reports would provide insights into the state of manufacturing activity and help shape expectations ahead of the upcoming jobs report on Friday.

In Japan, business sentiment improved in the second quarter, as indicated by the Bank of Japan’s quarterly Tankan survey.

The headline index for big manufacturers’ mood rebounded to +5 in June from +1 in the previous quarter, surpassing economists’ expectations.

China’s factory pace was very slow in June. The country’s manufacturing purchasing managers’ index fell to 50.5, down from 50.9 in May but slightly higher than economists’ expectations.

China’s official manufacturing PMI, reported by the National Bureau of Statistics, was at 49.0 in June compared to 48.8 in May, suggesting a contraction in the sector.

Looking at the performance of major U.S. stock indices, the Dow Jones Industrial Average gained 2.02% last week, marking its best weekly performance since March. The S&P 500 rose 2.35% and the Nasdaq Composite added 2.19%.

For the second quarter, the Dow climbed 4.56%, the S&P 500 increased by 8.30%, and the Nasdaq Composite gained 12.81%. Year-to-date, the Dow is up 3.80%, the S&P 500 has risen by 15.91%, and the Nasdaq Composite has surged by 31.73%, achieving its best first half since 1983.

Over the weekend, Tesla reported strong second-quarter vehicle production and delivery numbers.

The company delivered 466,140 vehicles and produced a total of 479,700, representing an 83% increase in deliveries compared to the previous year. This marks the fifth consecutive quarter that Tesla has produced more vehicles than it delivered.

- Published By Team Nation Press News